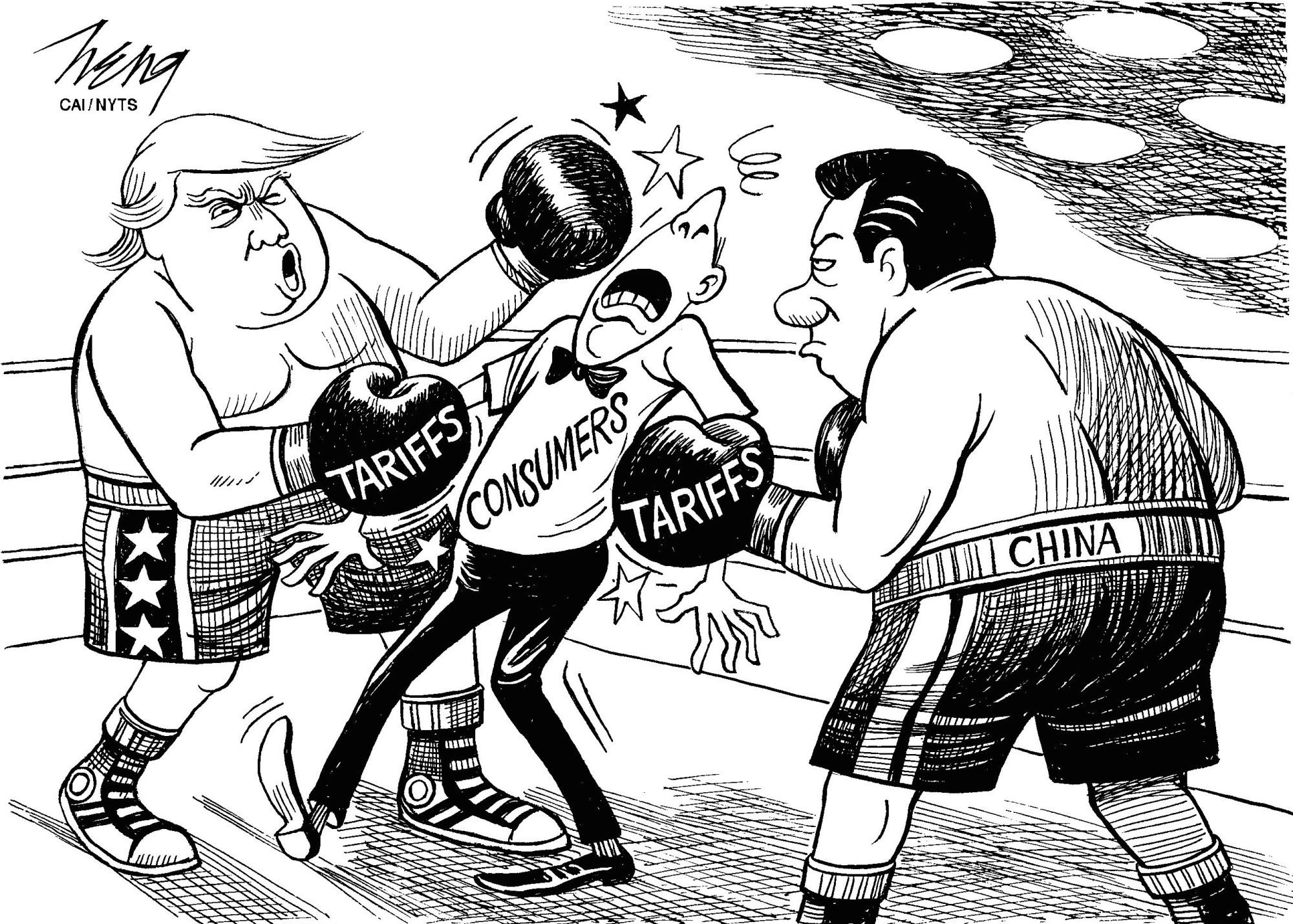

Dashing hopes of a quick agreement on trade relations with China, U.S. President Donald Trump's administration has imposed punitive tariffs on another $200 billion of Chinese goods. Now that the Chinese government has responded with new tariffs on $60 billion of U.S. products, the United States is threatening tariffs targeting yet another $300 billion of Chinese imports. Both sides are now digging in for a long fight — largely because Americans have yet to feel the pain of Trump's policies.

China has understood Trump's transactional style for some time. But it only recently began to appreciate fully the significance of Trump's "America First" doctrine, which according to U.S. State Department Policy Director Kiron Skinner, rests on four pillars: national sovereignty, reciprocity, burden-sharing and regional partnerships.

National sovereignty and reciprocity are standard features of any country's foreign policy. They form the foundations of the 1648 Peace of Westphalia, which recognized after the Thirty Years War that sovereign states have their own interests to defend and must engage with other states on a reciprocal basis.

, chief of staff for the 3rd Marine Division, bows in apology at the Okinawa Prefectural Government office in Naha on Thursday.")

and the staff of Oseto Suisan Fisheries prepare to check on their sustainably farmed fish.")

With your current subscription plan you can comment on stories. However, before writing your first comment, please create a display name in the Profile section of your subscriber account page.