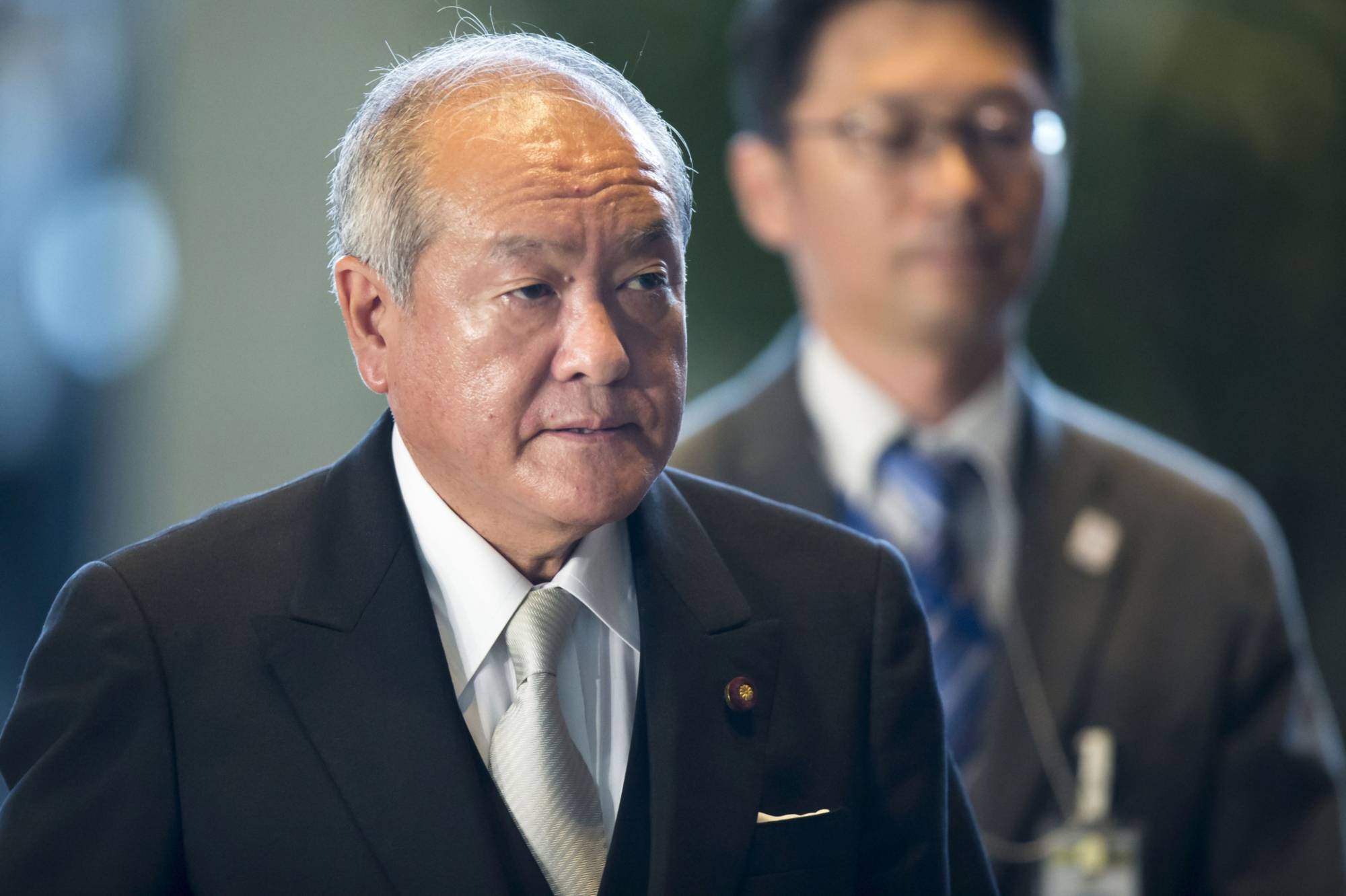

Former Olympics Minister Shunichi Suzuki on Monday became the first new finance minister in nearly nine years, replacing Taro Aso as the ruling party reboots its Cabinet in the run-up to a general election.

The 68-year-old Suzuki was appointed to the job after helping to install the country’s new prime minister, Fumio Kishida, who took the job earlier Monday. The son of a former prime minister, Suzuki belongs to a political faction headed by Aso and is also the out-going finance chief’s brother-in-law.

Because of those ties, Suzuki is viewed as a steward of the status quo, much like his boss, Kishida. He’s seen keeping the fiscal policies of recent years and continuing to support the Bank of Japan’s bond-buying and ultralow interest-rates, although there is speculation he might be susceptible to pressure to spend more.

, chief of staff for the 3rd Marine Division, bows in apology at the Okinawa Prefectural Government office in Naha on Thursday.")

and the staff of Oseto Suisan Fisheries prepare to check on their sustainably farmed fish.")

With your current subscription plan you can comment on stories. However, before writing your first comment, please create a display name in the Profile section of your subscriber account page.