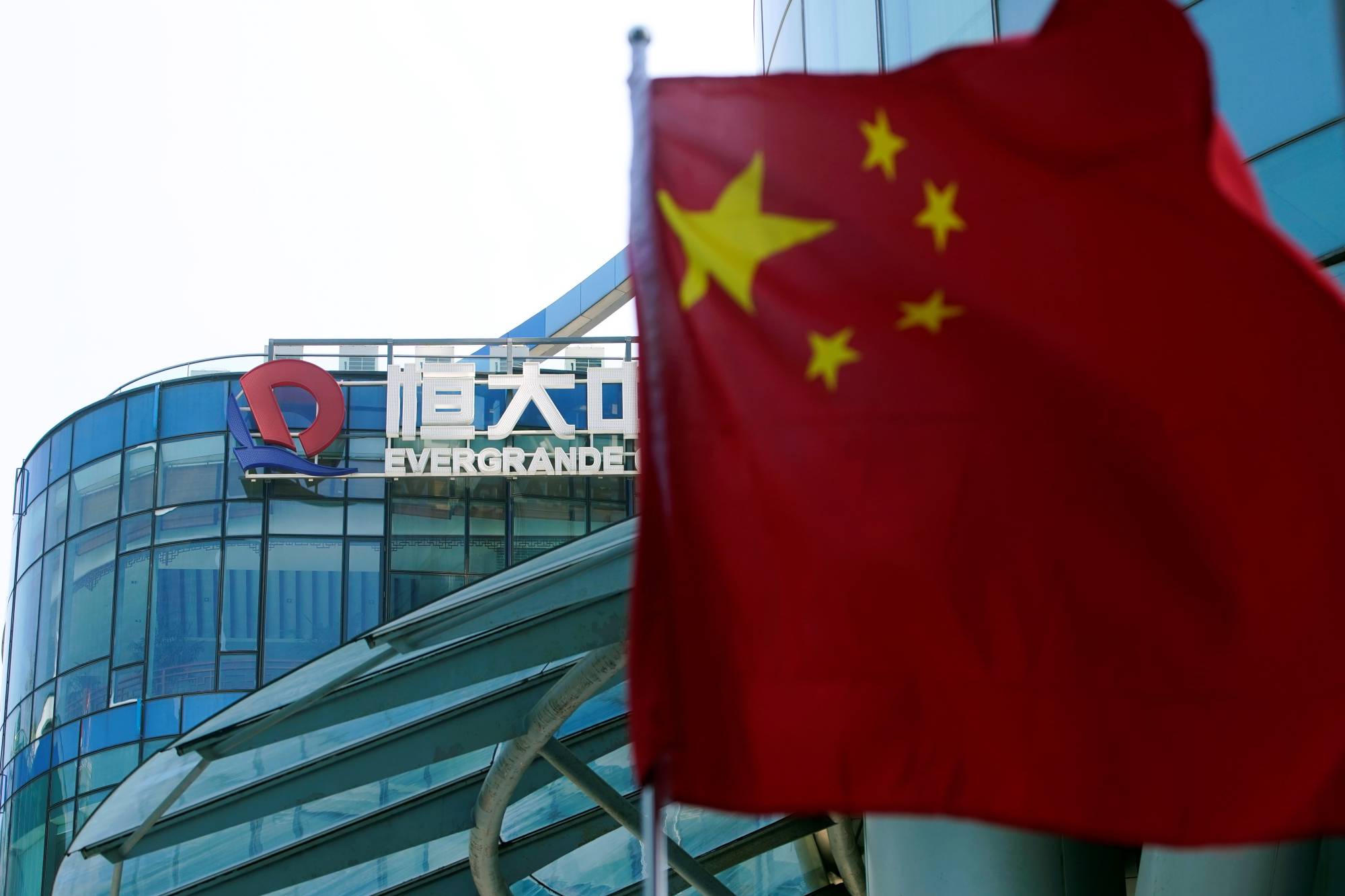

Wary of billion-dollar defaults, China does not want its daredevil real estate developers to take on any more debt.

Banks have been asked to limit their housing loan exposure, while developers that cross the so-called three red lines — a trio of leverage metrics Beijing watches — are forbidden from borrowing more.

Investors are clearly worried. China Fortune Land Development Co., a mid-sized developer, saw its dollar bonds tumble to record lows recently. How can home builders get out of their distress?

, chief of staff for the 3rd Marine Division, bows in apology at the Okinawa Prefectural Government office in Naha on Thursday.")

and the staff of Oseto Suisan Fisheries prepare to check on their sustainably farmed fish.")

With your current subscription plan you can comment on stories. However, before writing your first comment, please create a display name in the Profile section of your subscriber account page.