The Group of 20 summit in Argentina ended without fireworks involving the United States, which was appropriate in a way, given the pall cast by the death of President George H.W. Bush.

The U.S. went along with a watered-down communique rather than stand in the way of a consensus, as it recently did at the APEC summit and the Group of Seven. And rather than ending the meeting with a dramatic breakthrough or a loud breakdown, America reached an agreement to freeze trade tariffs with China that went somewhat beyond the one it reached with the European Union in July. Both deals require steadfast and detailed follow-through if the gains are to prove more than just temporary.

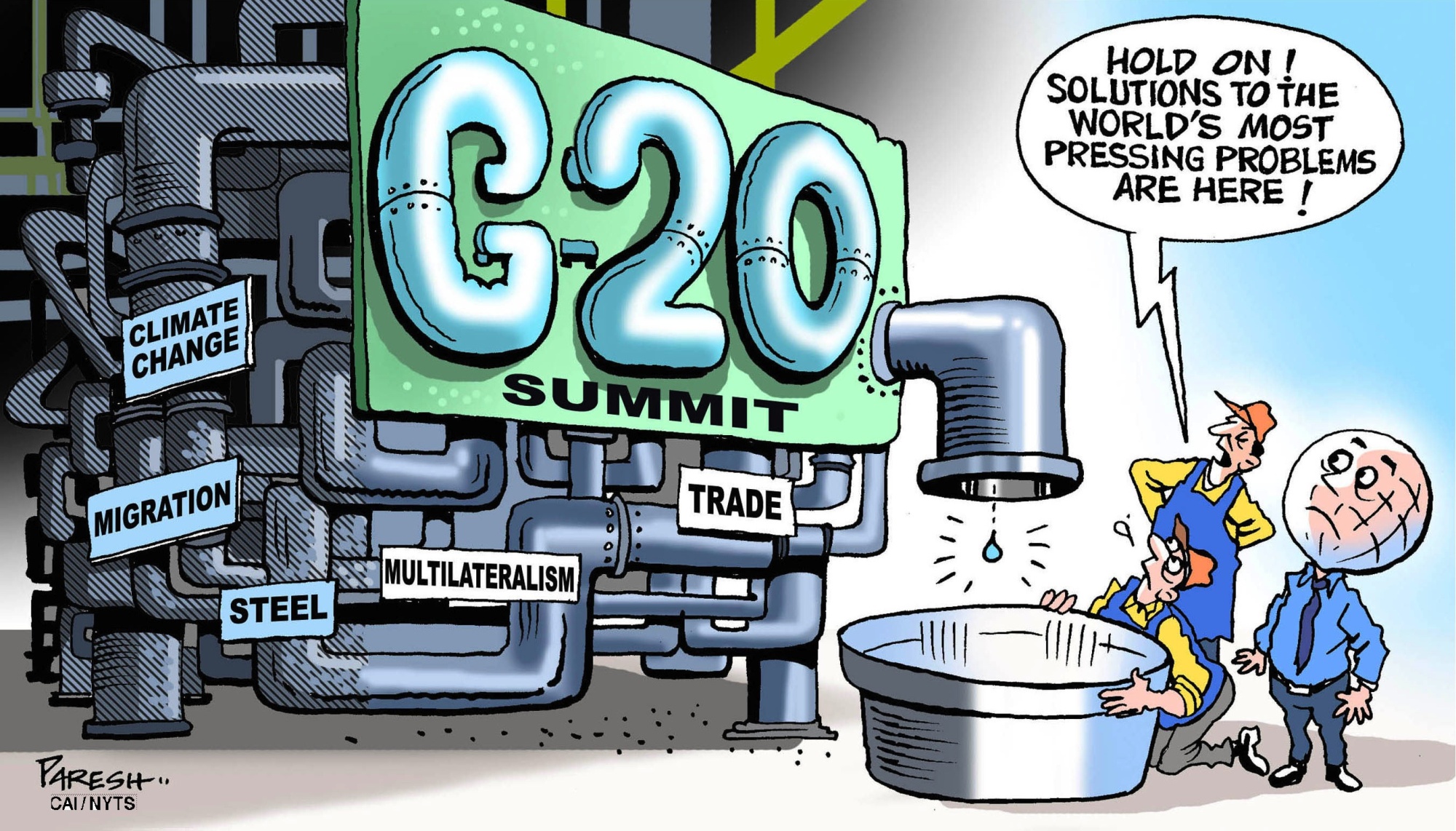

The expectations for the G20 summit were muted, with a balance of risk tilted to the downside.

, chief of staff for the 3rd Marine Division, bows in apology at the Okinawa Prefectural Government office in Naha on Thursday.")

and the staff of Oseto Suisan Fisheries prepare to check on their sustainably farmed fish.")

With your current subscription plan you can comment on stories. However, before writing your first comment, please create a display name in the Profile section of your subscriber account page.