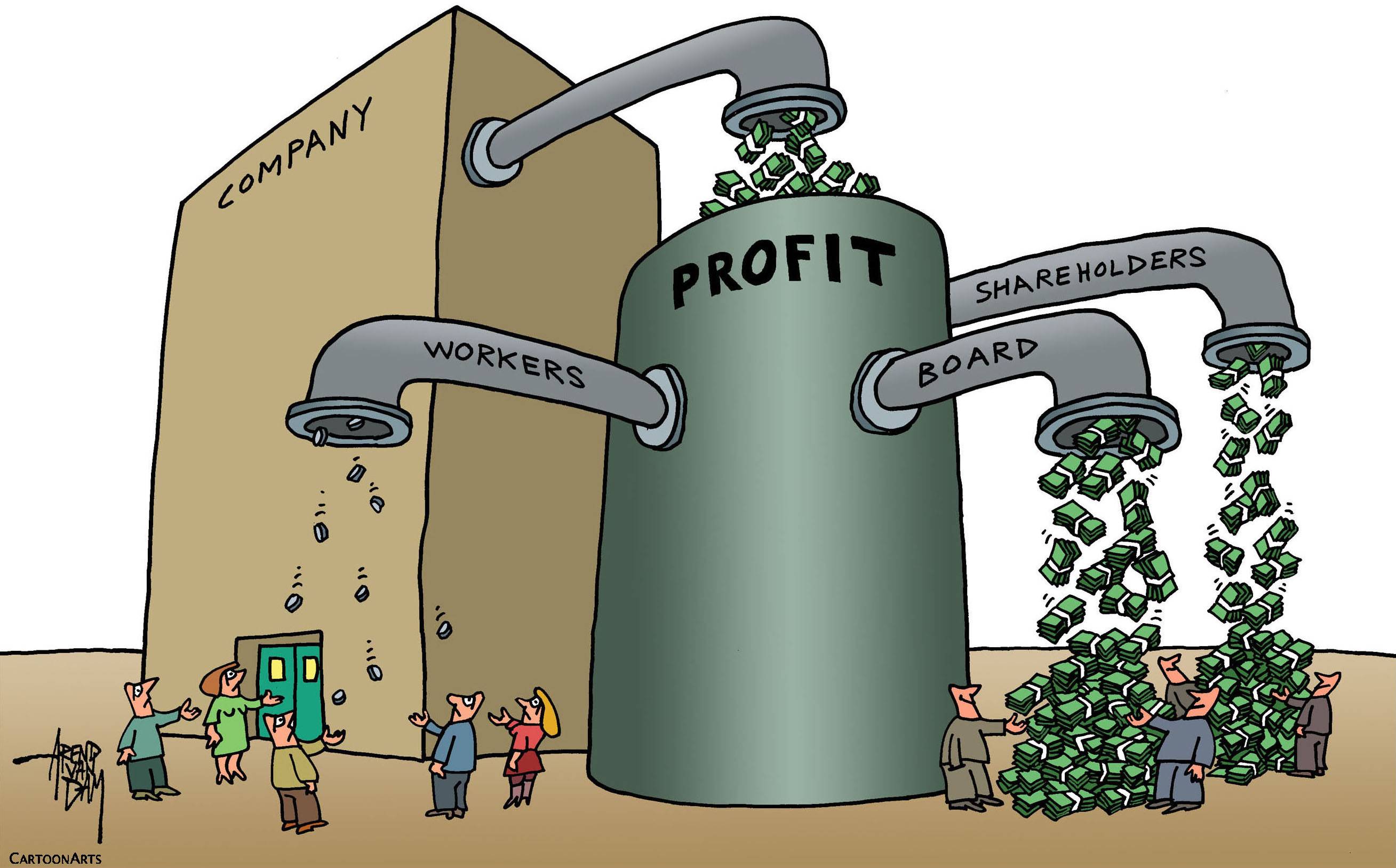

U.S.-style capitalism is at a major turning point. Last August, the Business Roundtable, an association of major companies in the United States, released the Statement on the Purpose of a Corporation, signed by 181 CEOs who committed to leading their firms for the benefit of all stakeholders: customers, employees, suppliers, communities and shareholders.

The statement represented a move away from “shareholder supremacy” and included a “commitment to all stakeholders.” It was akin to a collection of contracts signed by the top executives of U.S. firms such as JP Morgan Chase, Amazon, General Motors, etc., and its meaning was significant. In the U.S., which does not have a federal corporate law, Business Roundtable statements such as this are authoritative enough to have quasi-legal effects.

In 1997, the Business Roundtable issued a statement that corporations exist principally to serve shareholders. Therefore the significance and impact of last year’s statement to move away from shareholders is enormous. It supersedes the 1997 statement and outlines modern standards for corporate responsibility. It has the same purpose as recent amendments to corporate law in countries such as Britain and France, including “enlightened shareholder’s value” in Article 172 of the U.K. Companies Act 2006, the French PACTE Act in April 2019, and so on.

waves to attendees as he departs after delivering a campaign speech in Yokohama on Sunday.")

was included in the \"Continuity and Change\" exhibition that concluded in June.")

With your current subscription plan you can comment on stories. However, before writing your first comment, please create a display name in the Profile section of your subscriber account page.