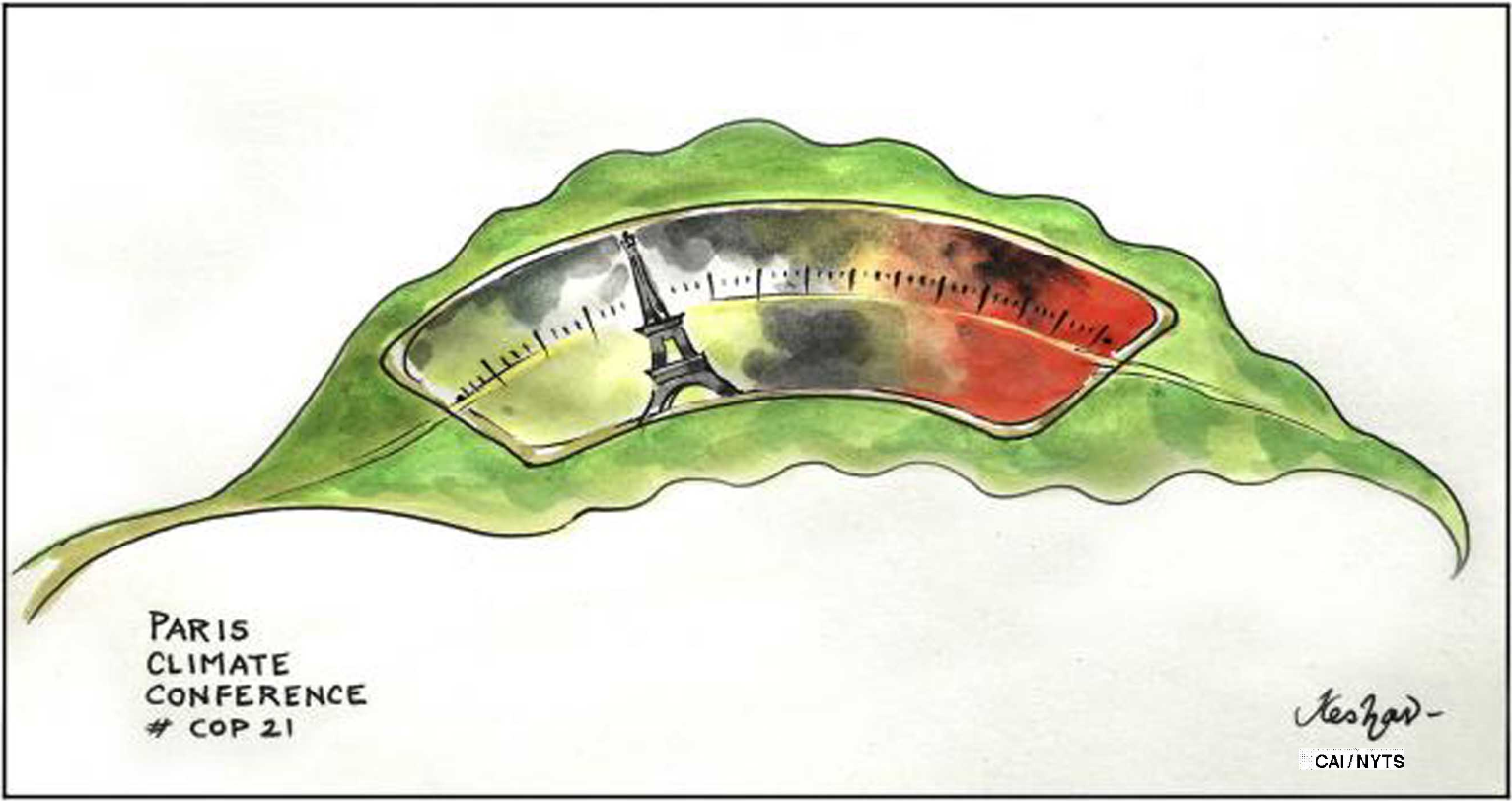

Last year, three facts about climate change became clear: Achieving a low-carbon economy is essential; new technologies make that goal attainable at an acceptable cost; but technological progress alone will be insufficient without strong public policies.

Extreme weather in December — big floods in South America, the United States, and Britain, and very little snow in the Alps — partly reflected this year's strong El Nino (caused by warmer Pacific Ocean water off Ecuador and Peru). But the planet's rising surface temperature will increase the probability and severity of such weather patterns, and 2015 — the warmest year on record — confirmed that human greenhouse-gas emissions are driving significant climate change. Earth's average land surface temperature is now about 1 degree C above preindustrial levels.

Faced with that reality, the climate agreement reached in Paris last month represents a valuable but still insufficient response. All major economies are now committed to reducing emissions below business-as-usual levels: but the combination of national commitments would likely result in warming of almost 3 degrees above preindustrial levels — a terrifying prospect, given the adverse consequences already apparent from a 1-degree rise.

in Yokohama on Sunday.")

and Commerce Secretary Howard Lutnick at Morristown Airport, New Jersey, on Sunday. Trump on Monday sent letters to 12 countries notifying them of new \"reciprocal\" tariff rates effective Aug. 1.")

and Hifumi Abe (second from right) with their brother Yuichiro (center) and their parents. “I’m always consciously trying to be a good older brother,” Yuichiro said.")

With your current subscription plan you can comment on stories. However, before writing your first comment, please create a display name in the Profile section of your subscriber account page.