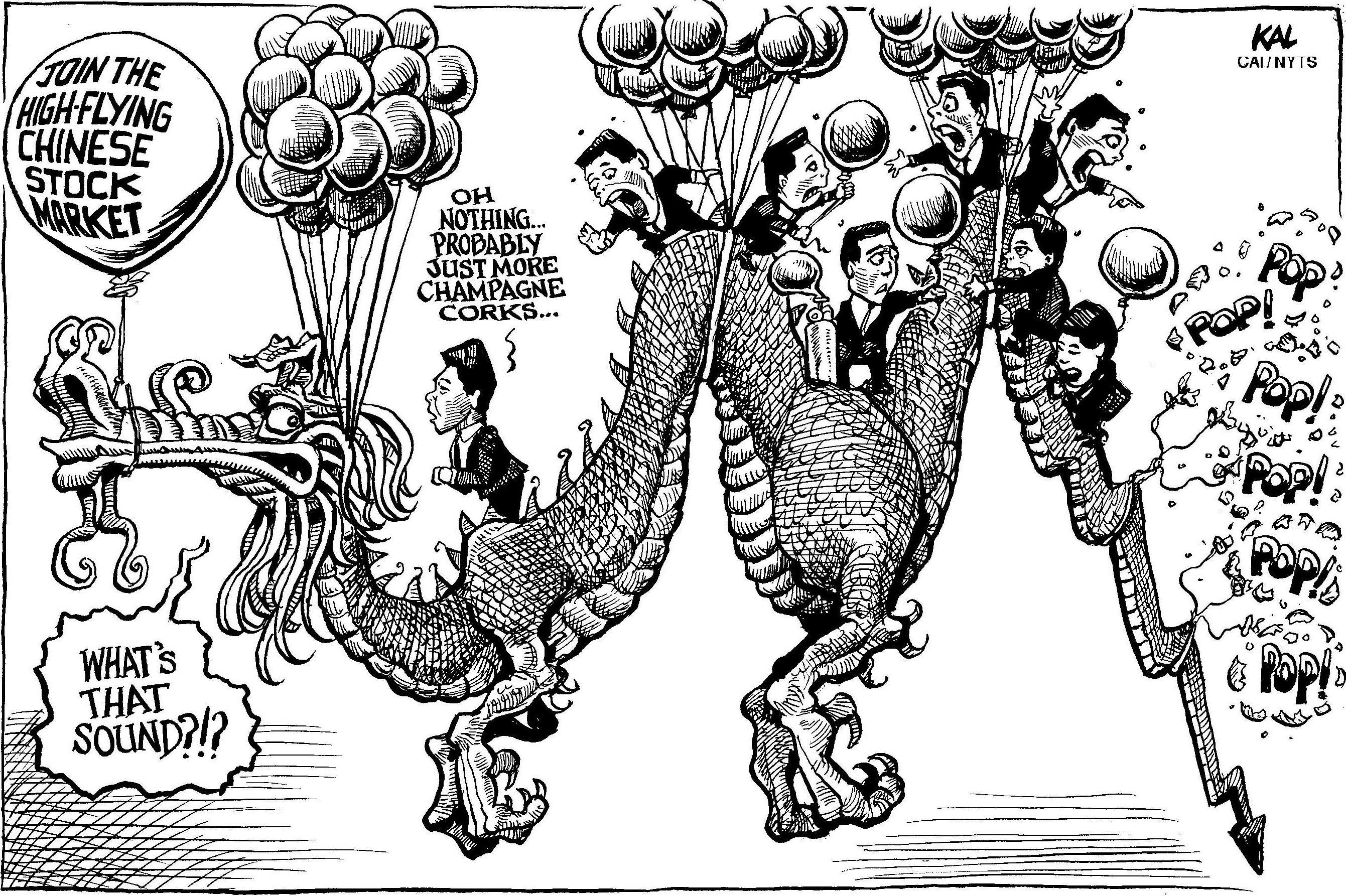

When the United States sneezes, an old saying goes, the world catches a cold. That's been nowhere more true than in Asia. But as China's coughing fit grows louder, countries in the region are wondering whether their neighbor's illness will also prove contagious.

Since Wall Street's crash in 2008, Asia has been pivoting to China. The $16.8 trillion U.S. economy is still 1.8 times bigger and its per capita income dwarfs China's. But China is Asia's biggest trading partner and, increasingly, its benefactor. Flush with $3.7 trillion of currency reserves and its new $100 billion Asian Infrastructure Investment Bank, China has used checkbook diplomacy to make friends across the region.

Asia's social media accounts are now pulsating with talk of how a #ChinaMeltdown might send the region into a tailspin. Even Australia, which is reeling from plunging iron ore prices, and Japan, whose currency is suddenly surging, are bracing for a downturn. As China's high-flying economy confronts the basic laws of economics and finance, many countries in Asia are second-guessing the relationships they established with Beijing in better times.

waves to attendees as he departs after delivering a campaign speech in Yokohama on Sunday.")

, performing with Connor Walsh as Albrecht, is one of six Japanese dancers at Houston Ballet.")

and Hifumi Abe (second from right) with their brother Yuichiro (center) and their parents. “I’m always consciously trying to be a good older brother,” Yuichiro said.")

With your current subscription plan you can comment on stories. However, before writing your first comment, please create a display name in the Profile section of your subscriber account page.