U.S. President Barack Obama has declared the economic crisis over — and for the United States, maybe it seems that way. But for most other countries, not so much. Their recoveries are faltering. The obvious question is whether the global weakness will infect the U.S. expansion. This is a crucial footnote to Obama's optimism.

Two major reports — one from the World Bank, the other from its sister organization, the International Monetary Fund — recently lowered estimates for global economic growth in 2015. Said the IMF: "The United States is the only major economy for which growth projections have been raised."

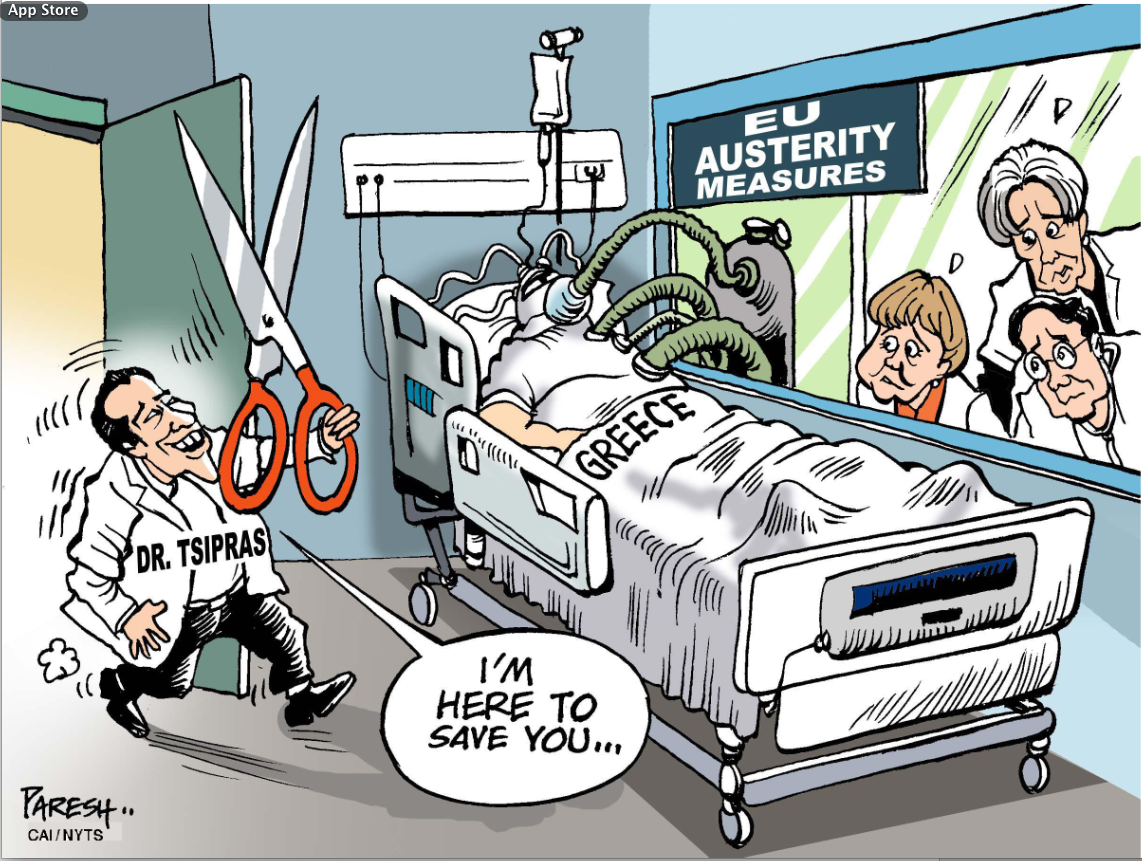

Consider the bleak landscape. Japan is in recession. Unemployment in the euro zone (the 19 countries using the euro) is a scary 11.5 percent. Unhappily, the IMF expects only meager euro-zone growth of 1.2 percent in 2015. Even this could be optimistic if the Greek election triggers a new debt crisis. Assuming the IMF forecast is reached, growth would still be a third of the predicted U.S. rate (3.6 percent).

waves to attendees as he departs after delivering a campaign speech in Yokohama on Sunday.")

, performing with Connor Walsh as Albrecht, is one of six Japanese dancers at Houston Ballet.")

and Hifumi Abe (second from right) with their brother Yuichiro (center) and their parents. “I’m always consciously trying to be a good older brother,” Yuichiro said.")

With your current subscription plan you can comment on stories. However, before writing your first comment, please create a display name in the Profile section of your subscriber account page.